Bank Mandiri: Indonesia's #2 bank at 4.8x earnings - 18% profit growth, ~9% net dividend, 2.8%/yr currency hedge

Bank Mandiri (IDX: BMRI) fits a profile that has historically produced outsized returns on frontier markets: the leading bank of a fast-growing economy, trading at 4.8x earnings with a double-digit dividend yield and accelerating growth. This review is built on primary filings - consolidated IFRS statements and the monthly bank-only disclosures mandated by Indonesia's regulator OJK.

The #2 bank of the world's 4th most populous country

Mandiri is a state-controlled (52%) universal bank with roughly IDR 2,300 trillion (~$130bn) of bank-only assets. Indonesia has 280+ million people, banking penetration well below regional peers, and ~9-10% nominal GDP growth (5% real plus ~3% inflation). Unlike its retail-focused state peers, Mandiri is the wholesale champion (Kopra corporate platform) with a fast-scaling retail super-app (Livin'). Cheap current-and-savings accounts fund 71.6% of the balance sheet.

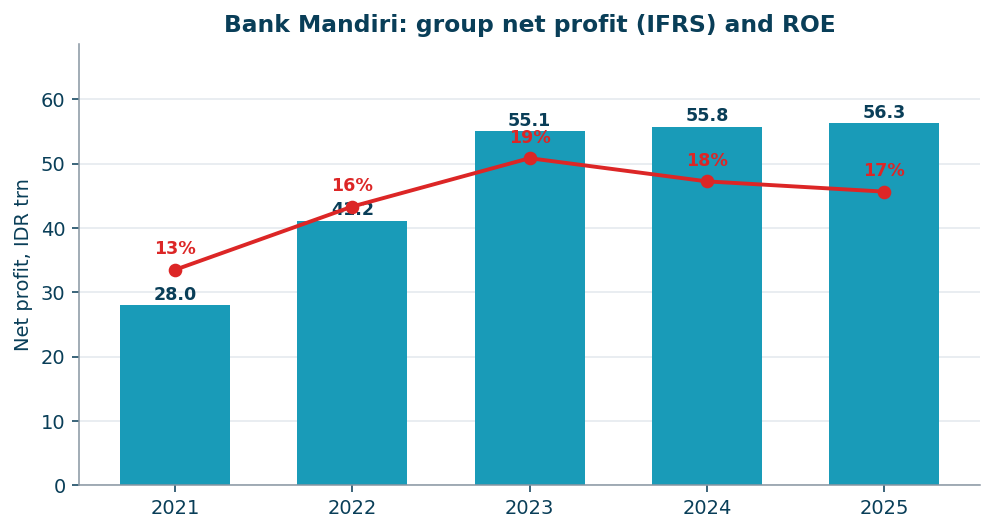

Profit doubled in four years; ROE ~20%

Group IFRS revenue grew from IDR 86.6trn in 2021 to 144.8trn in 2025; net profit doubled from 28.0trn to 56.3trn. ROE rose from 12.6% to 17-19%, and printed 20.4% in Q1 2026. Management targets sustainably above 20%.

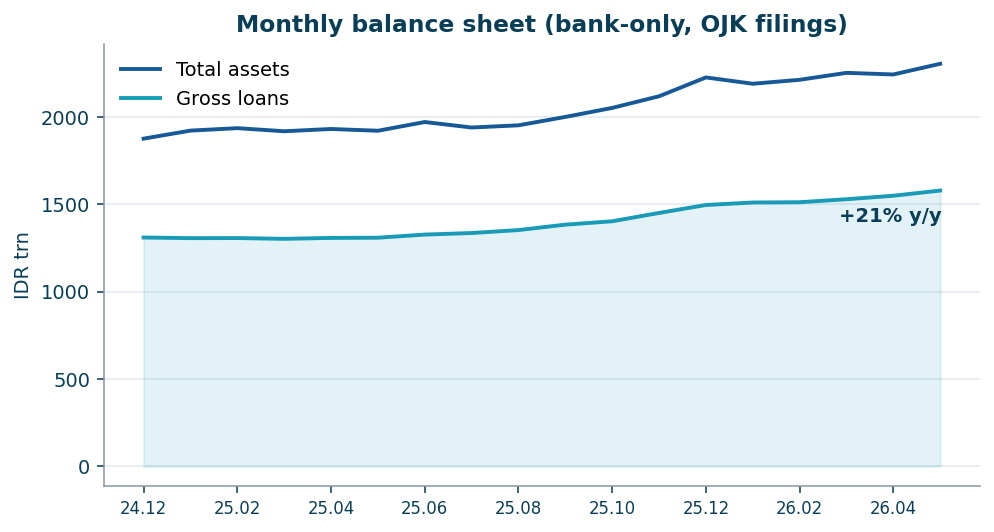

Monthly regulatory data: growth is accelerating, not slowing

Indonesian banks publish monthly balance sheets and P&L (an OJK requirement). As of May 2026 (bank-only): loans +20.6% y/y, assets +20%, deposits +22%, five-month net profit +18.3% y/y with impairments down 16%. Every month of 2026 has printed double-digit profit growth over the same month of 2025.

One nuance only visible in monthly data: net interest income grows slower than loans (+10% vs +21%) as time deposits (+57% y/y) outpace cheap CASA - the reason management trimmed 2026 NIM guidance to 4.5-4.7%.

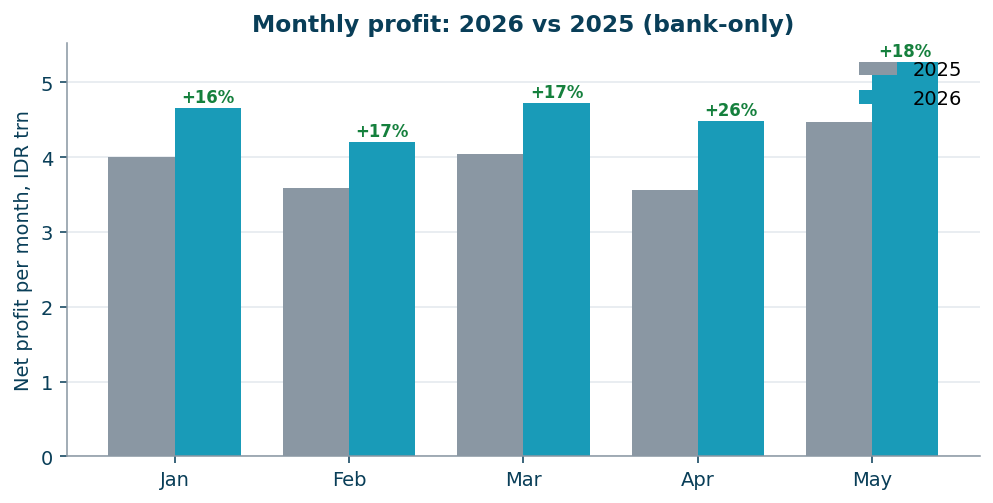

The Q1 2026 asset 'shrinkage' is an accounting event, not the business

Consolidated assets fell from IDR 2,830trn to 2,433trn in Q1 2026. The cause is the deconsolidation of sharia subsidiary BSI (IDR 456trn of assets): its golden share moved to sovereign fund Danantara on 23.01.2026, and the stake became a financial investment. Dividends are irrelevant here - the IDR 35.1trn payout hit equity in April. Consolidated y/y comparisons will look depressed through 2026; the clean monthly bank-only series shows +20% growth.

2026 guidance: loans +7-9%, credit cost 60-80bp, payout 65-70%

Management guides loans +7-9% (running above), NIM 4.5-4.7% (Q1: 4.7%), cost of credit 60-80bp (gross NPL 0.98%, net 0.41%), CIR ~40%, ROE above 20%, dividend payout 65-70% of profit.

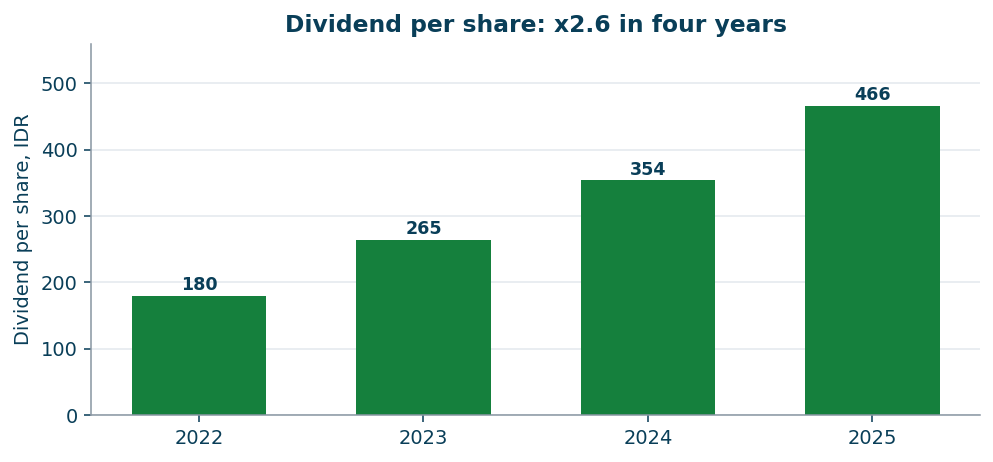

Dividend per share tripled in four years; ~11% gross yield

The approved FY2025 payout is 70% of profit (IDR 44.5trn): a Rp100 interim (January 2026) plus a Rp376.96 final dividend - roughly 11% on the current price. The controlling shareholder, sovereign fund Danantara, is institutionally pushing payout ratios up across state banks. Non-resident withholding tax is 20% (for jurisdictions without a treaty), leaving ~9% net.

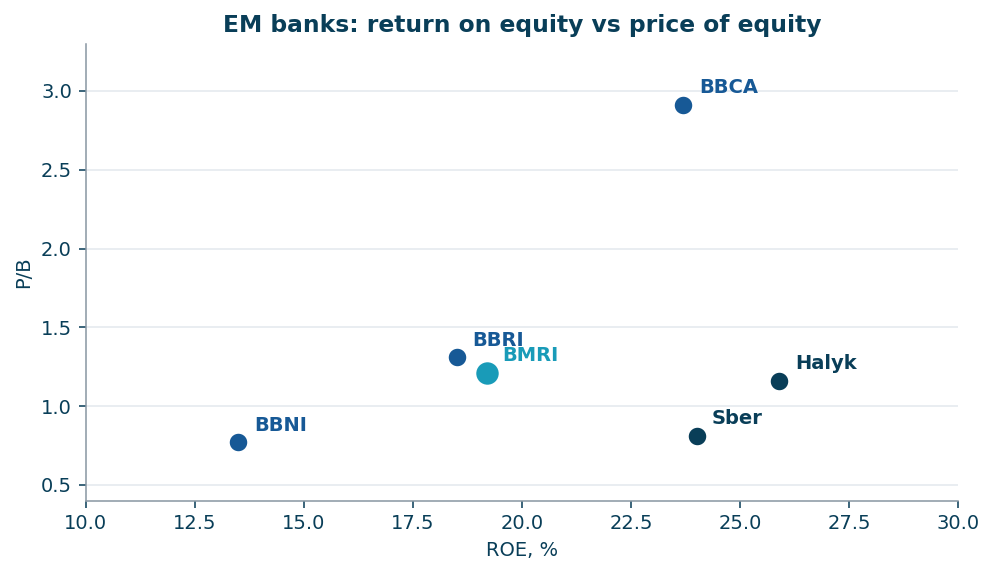

Valuation: 20%-ROE capital at 1.2x book

P/E 4.8, P/B 1.21 at ~19-20% ROE. A sustainable-growth cross-check: with 20% ROE, ~9% growth and even a stressed 16% cost of equity, fair P/B is ~1.6 - roughly 30-40% upside before any re-rating of the country discount. Local brokers carry IDR 5,700 targets (1.7x book). Within the same sector, privately-owned Bank Central Asia trades at 2.9x book on a 23.7% ROE - a measure of the discount embedded in state banks.

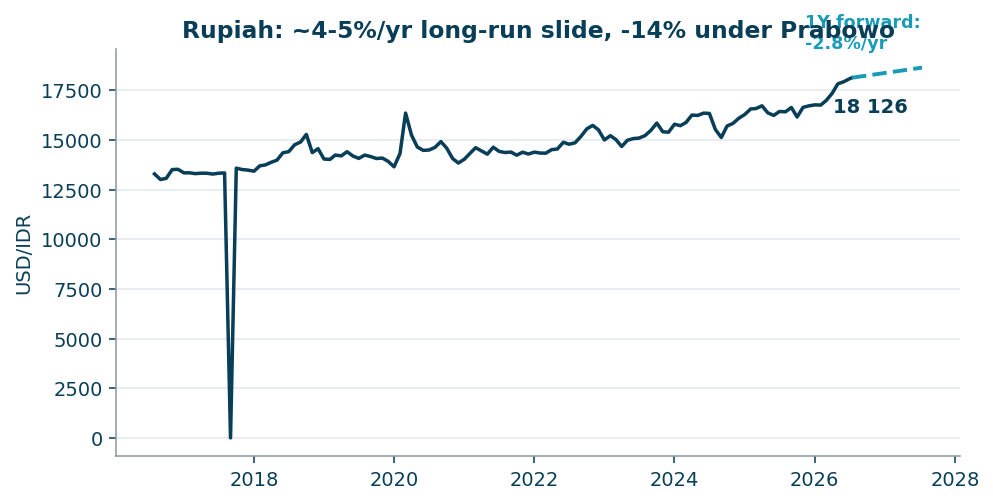

The rupiah: -14% under the new president, hedgeable at 2.8%/yr

Rupiah depreciation is historically moderate and gradual: ~4.7%/yr over 5 years, ~3.1%/yr over 10, with no one-day collapses (unlike the tenge or rouble). The last year brought a -10% acceleration on capital outflows: finance minister Sri Mulyani's dismissal, opaque governance at Danantara, and fiscal expansion. Bank Indonesia defends the currency at a 5.75% policy rate against 3.3% inflation (+2.4% real), and the forward market prices just 2.8% annual depreciation - the position's currency risk can be insured for a quarter of the dividend. For comparison: hedging the rouble costs ~9%/yr, the tenge ~13%/yr.

Versus Halyk and Sberbank: the best hedged-USD expected return

Halyk (P/E 3.8, ROE 26%, ~11% net dividend) prints -4% y/y profit for 5M2026 under tighter reserve requirements and retail lending rules, while the tenge has appreciated ~18% in real terms over a year with a prohibitive ~13% hedge cost. Sberbank (P/B 0.81, ROE 24%) grows profit +20% y/y, but the rouble hedge costs ~9%/yr and the currency sits at multi-year real highs. Mandiri is the only one of the three combining positive profit momentum with a cheap hedge: ~9% net dividend + ~10% EPS growth - 2.8% hedge = ~15-16% expected USD return with currency risk closed.

Risks

Danantara governance (the same control that lifts payouts can direct banks into policy programmes); directed lending (the $12bn village-cooperative scheme mostly burdens retail-focused BBRI, but the perimeter can widen); NIM pressure from expensive time deposits; depreciation above forward rates if outflows persist; and the 20% dividend withholding for most non-residents.

How to buy

The practical route for international investors is the unsponsored ADR PPERY (US OTC): available at Interactive Brokers at standard US commissions (~$0.005/share), ~$1.6m average daily turnover - comparable to Halyk's LSE GDR. Use limit orders only (OTC spreads); the depositary deducts ~$0.01-0.05/share/yr from dividends. Direct Jakarta listing BMRI.JK for those with IDX access.

Prepared by Eninvs (July 2026) from Bank Mandiri's IFRS statements, OJK monthly filings, KASE, CBR, MOEX and national-regulator data. Not investment advice.