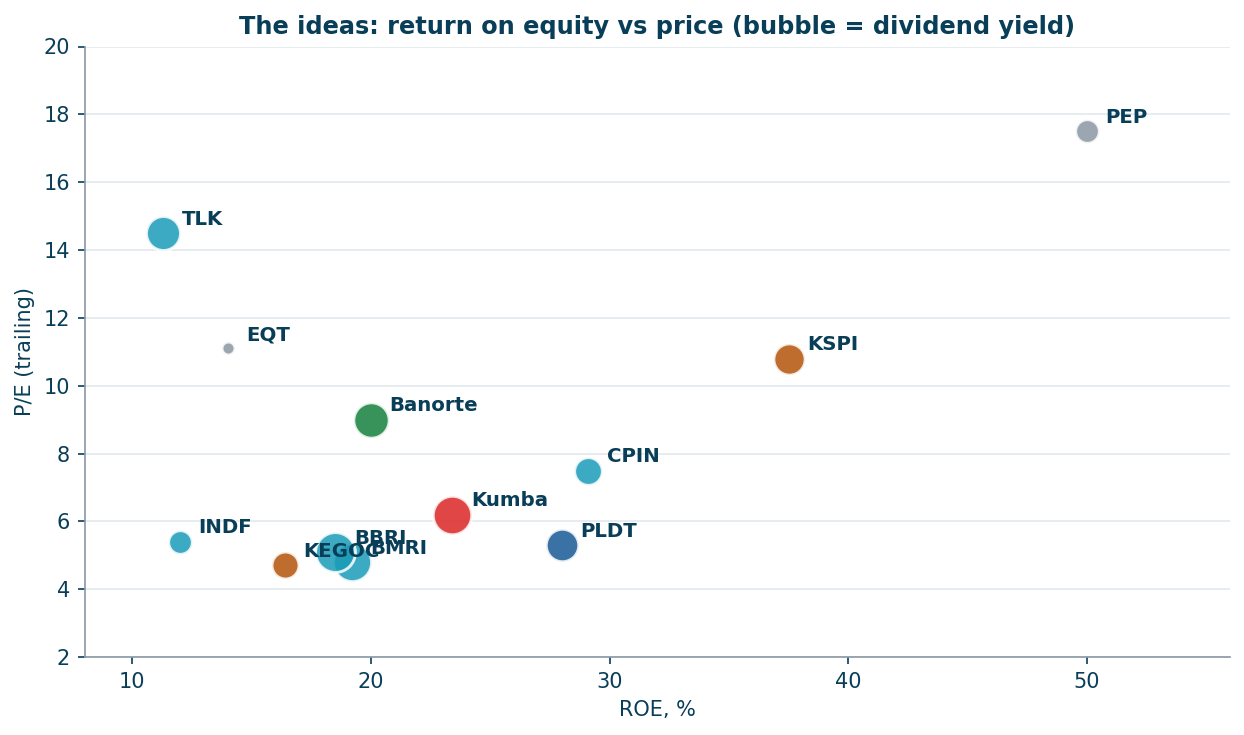

13 investment ideas across frontier markets, commodities and US leaders - July 2026

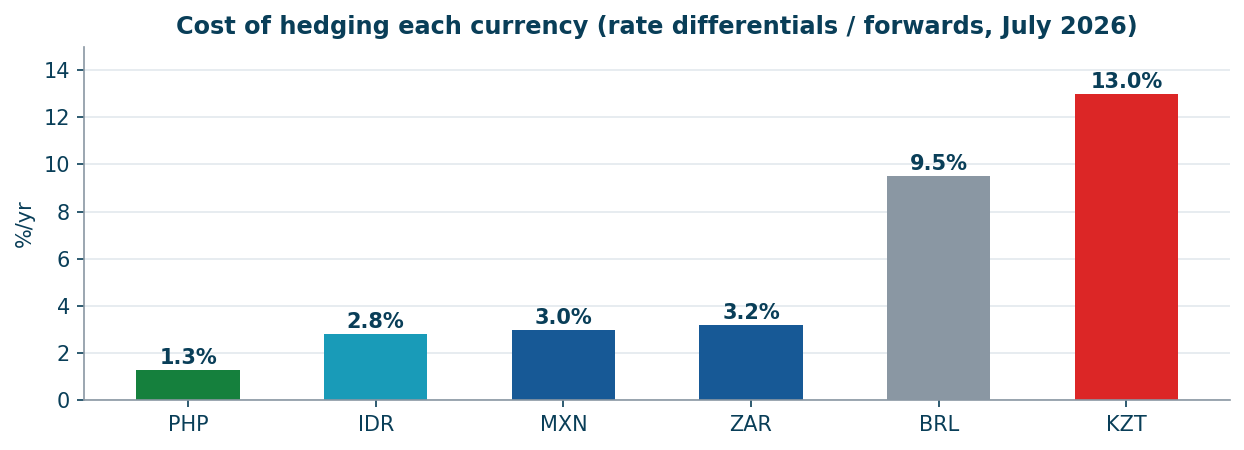

Thirteen ideas from our coverage across frontier markets, commodities and US large caps. Each was produced by one of five live engines (EM bank value with monthly regulatory data, EM compounders, dividend+catalyst, commodity spot mean-reversion, US Leaders GARP), screened across ~500 issuers and verified against primary filings. Currency math is a first-class criterion: a 12% dividend behind a 13%/yr hedge is worth less than 9% behind a 2.8% one.

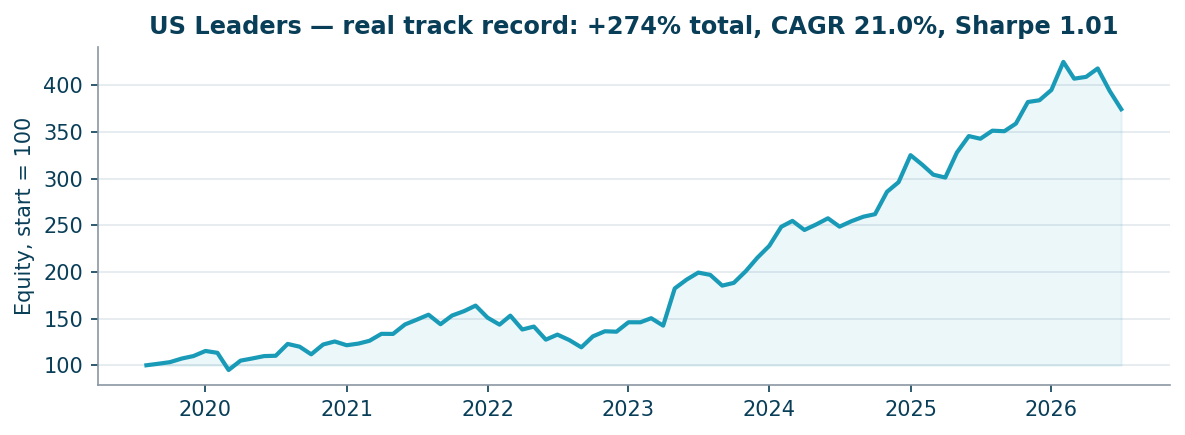

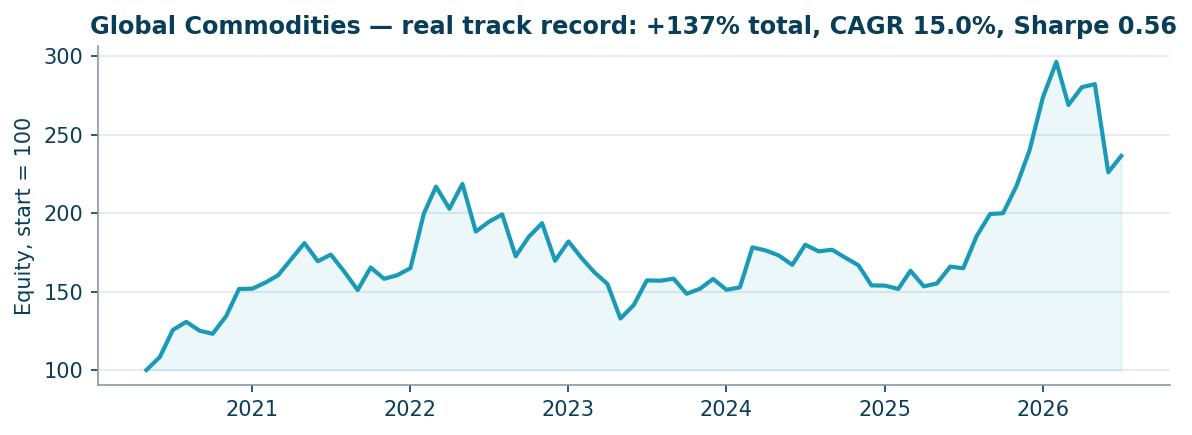

Live track records of the two systematic books contributing ideas: US Leaders +274% since Aug 2019 (CAGR 21%, Sharpe 1.0); Global Commodities +137% since May 2020 (CAGR 15%). The commodity engine's latest published call - PBF at $42 on June 25 - is +36%.

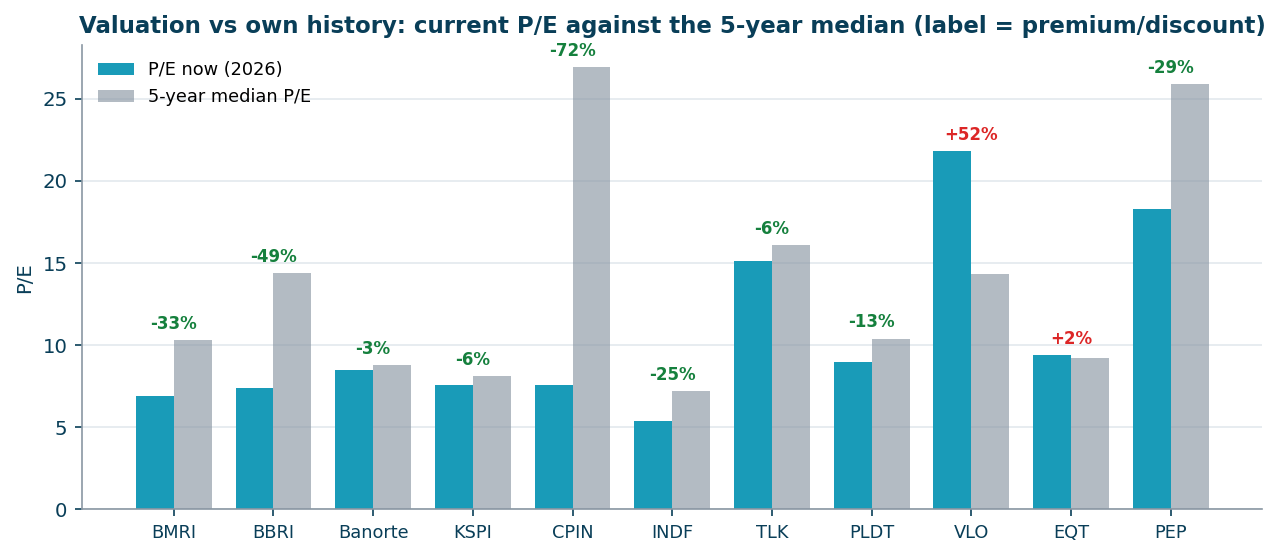

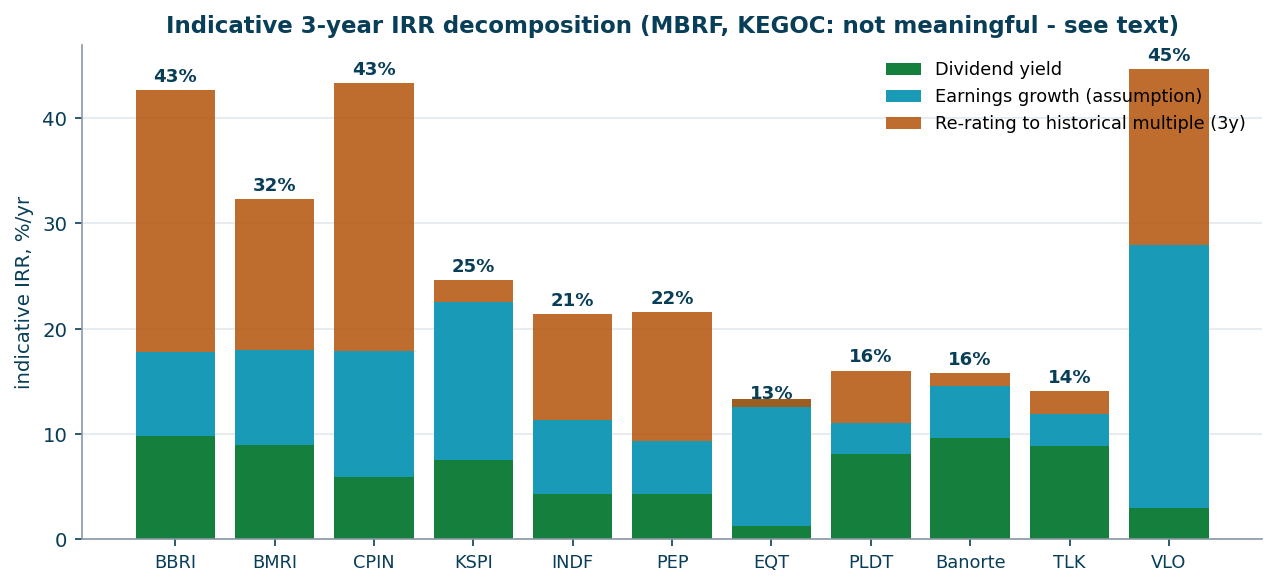

The numbers layer: valuation vs history and an indicative IRR sketch

Is each name cheap against ITS OWN history, and what annual return does the position imply if the multiple drifts back to the 5-year median while the business grows and pays out? Charts below; per-name assumptions in the cards. Growth assumptions are deliberately conservative vs recent prints; CPIN capped at 15x; VLO on forward earnings; MBRF and KEGOC excluded as not meaningful.

Part I. EM bank value

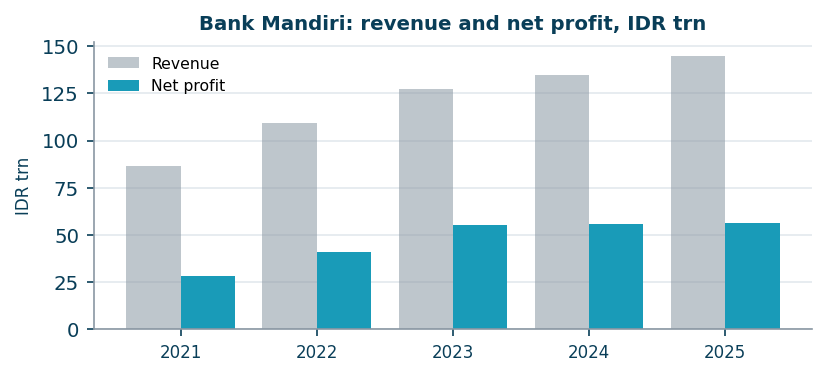

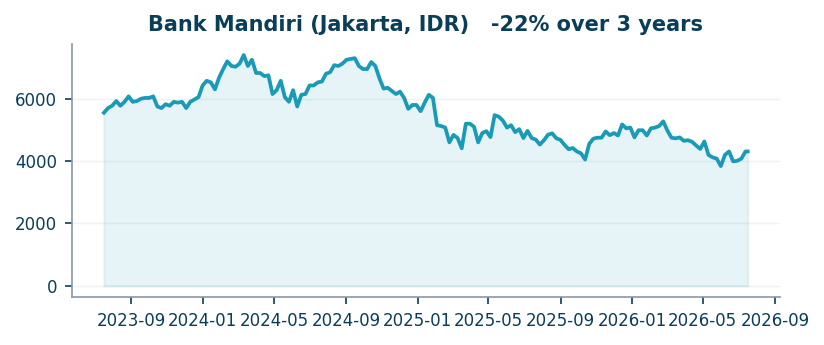

1. Bank Mandiri (IDX: BMRI; ADR PPERY) - the flagship

Indonesia's #2 bank: wholesale-led franchise, 71.6% CASA funding, ROE 20.4% in Q1'26, monthly regulatory data showing acceleration. Expected hedged USD return ~15-16%/yr before re-rating. The Q1 consolidated 'asset shrinkage' is the BSI deconsolidation, not the business. Risks: Danantara governance, directed lending, NIM pressure.

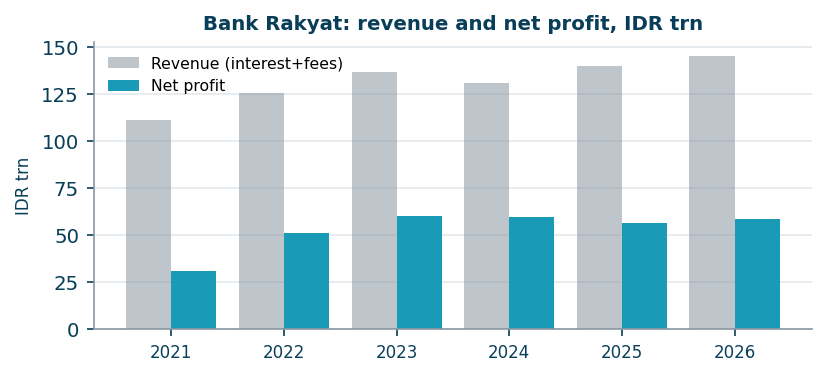

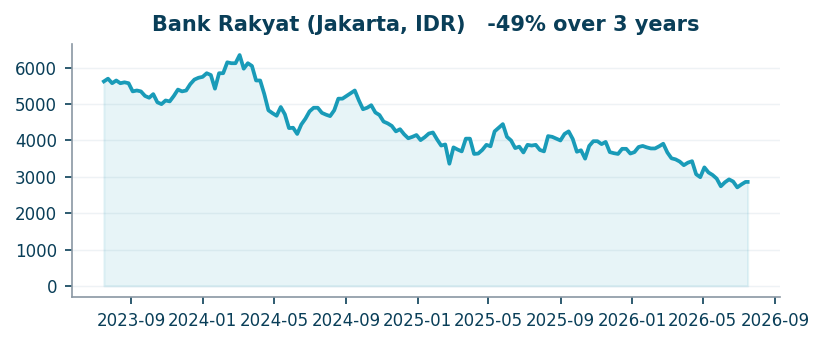

2. Bank Rakyat (IDX: BBRI; ADR BKRKY) - the higher-yield pair

The world's largest microlender (65m borrowers). 2025 was the clean-up year; the cycle is turning. With Mandiri - a sector bet at ~5x earnings with double-digit dividends. Risk: BBRI carries most of the $12bn village-cooperative programme.

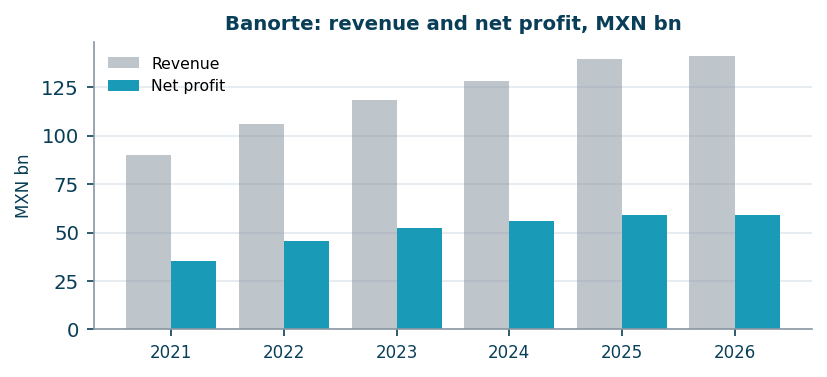

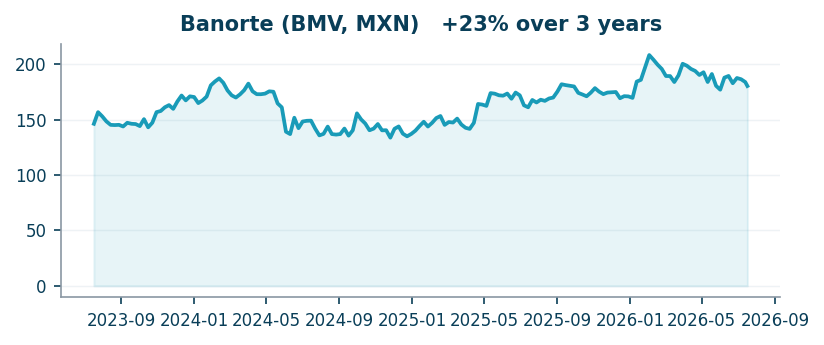

3. Banorte (BMV: GFNORTEO) - the dividend machine with direct access

Mexico's #2 financial group: a durable ~10% peso cash yield from a franchise that survived every Mexican cycle since 1899; nearshoring optionality is free. Risks: Banxico cuts, US-Mexico politics.

Part II. EM compounders

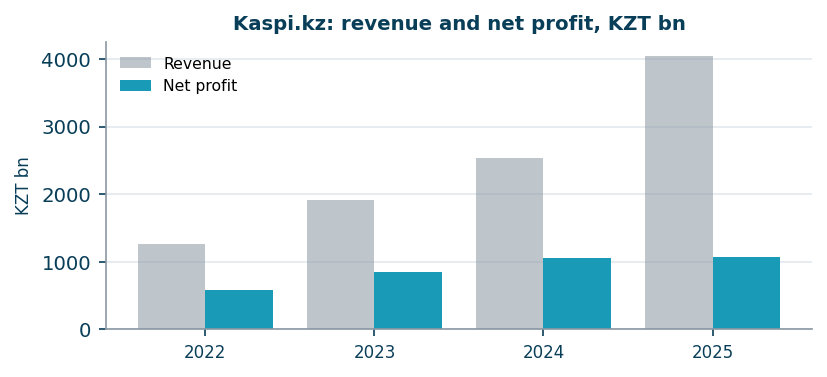

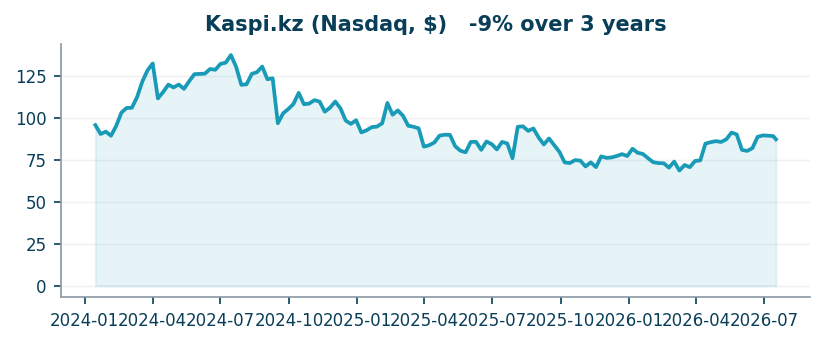

4. Kaspi.kz (Nasdaq: KSPI) - quality growth at a value price

Kazakhstan's payments+marketplace+fintech monopoly funding a second act in Turkey (Hepsiburada) from its own cash flow. If Turkey works - a second engine; if not, the core justifies the price. Risks: tenge, fee regulation, Turkish execution.

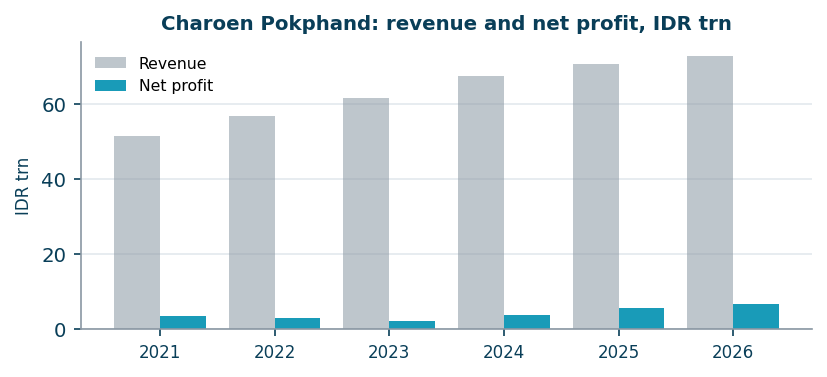

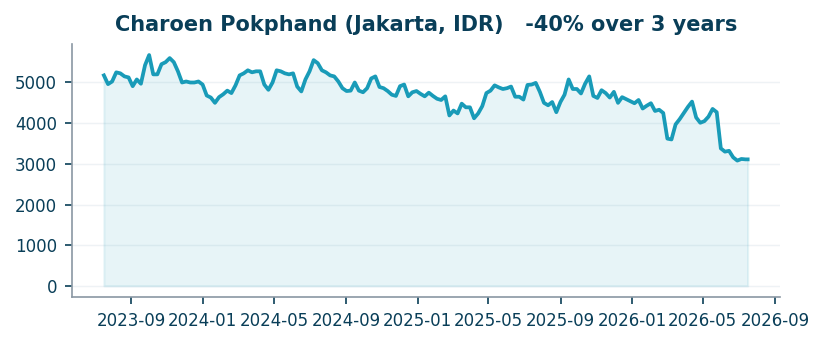

5. Charoen Pokphand Indonesia (IDX: CPIN) - protein for 280 million people

Indonesia's poultry leader. The free-school-meals programme that worries bank investors adds 5-7% to broiler demand - a natural internal hedge in an Indonesian basket. Margins will normalize; the per-capita protein story is early. Risks: feed costs, normalization.

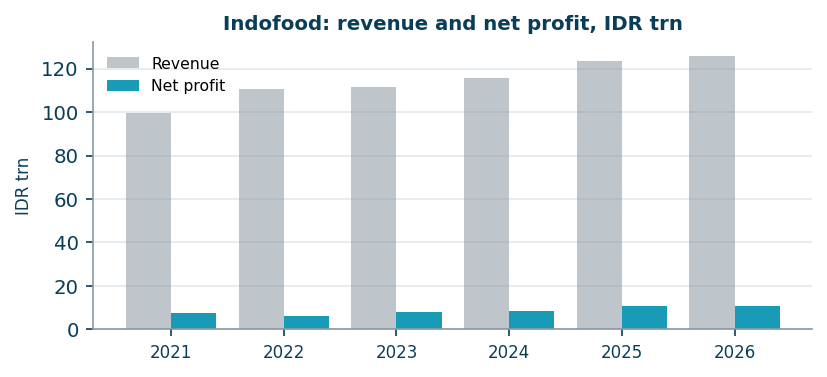

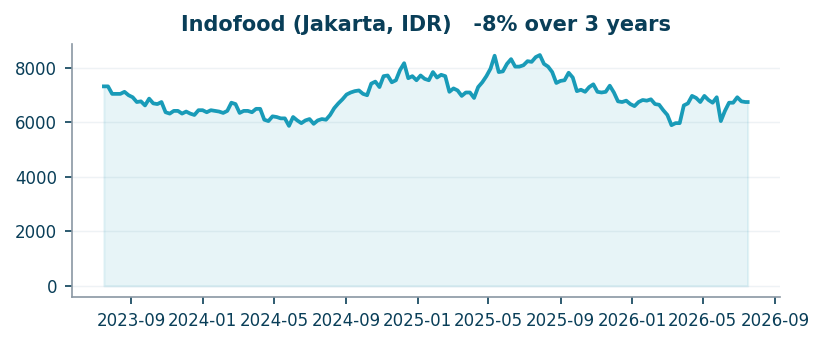

6. Indofood (IDX: INDF) - the Indomie monopoly at half book

Indomie is close to a de-facto noodle monopoly and one of Asia's most recognizable brands. The discount is structural (holding, country), not operational. Risks: holding discount persistence; wheat/palm oil.

Part III. Dividend + catalyst

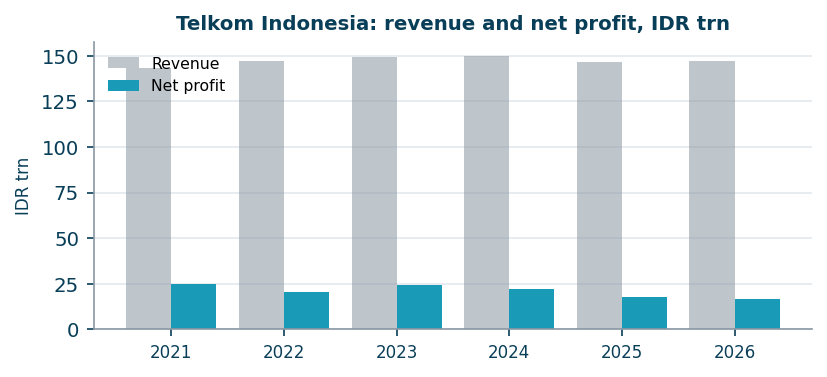

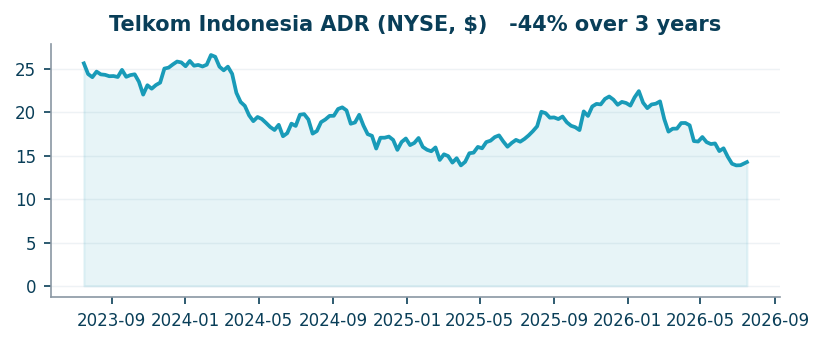

7. Telkom Indonesia (NYSE: TLK) - value with a spin-off attached

Indonesia's incumbent telecom after a governance reset. Tower/data-center carve-outs have historically unlocked value across Asian telecoms; here one comes with a 9% yield attached. Risks: price war, timelines.

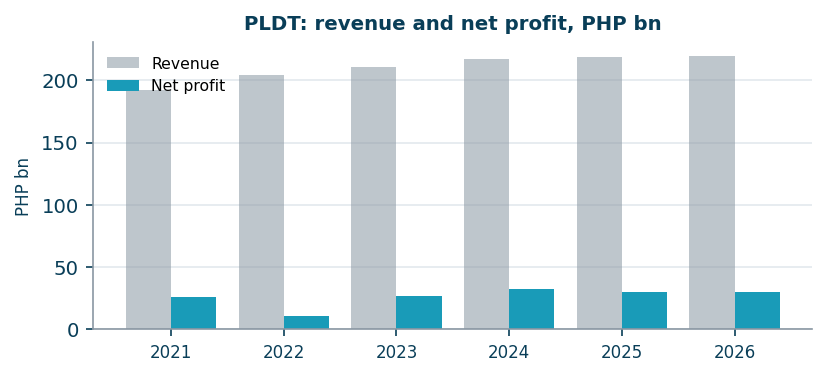

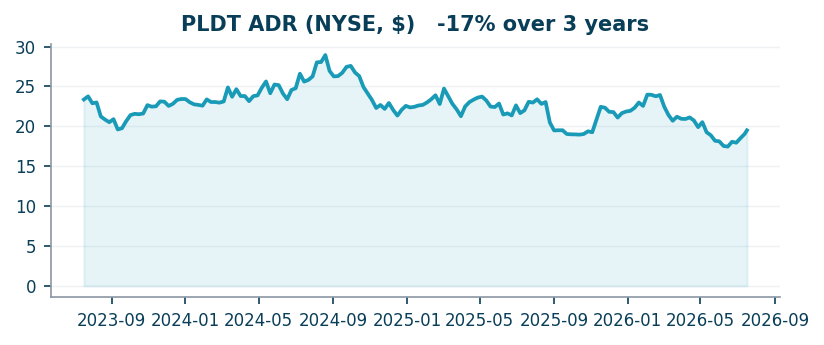

8. PLDT (NYSE: PHI) - dividends plus a free fintech option

The Philippine telecom leader whose #2 digital bank the market values at zero. Capex peak passed, FCF positive, deleveraging to 2.0x. Risk: leverage 2.56x EBITDA - the highest here.

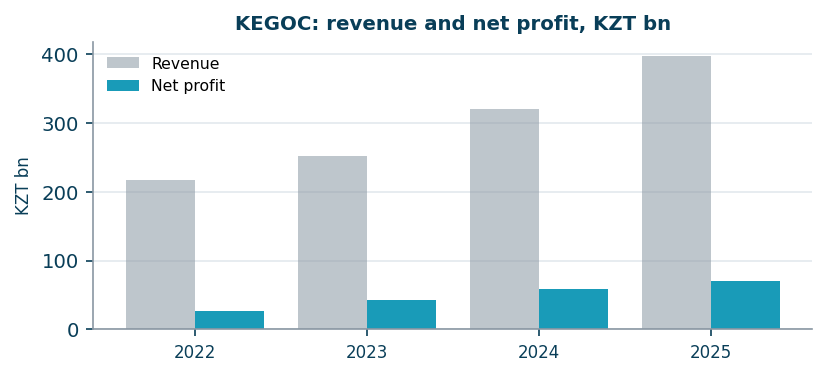

9. KEGOC (KASE: KEGC) - the grid monopoly after a tariff reset

Half of book value for the national grid with regulated returns flowing through. Last despite best momentum: currency and access fail the USD framework; strong local-book idea. Risk: tariff politics.

Part IV. Commodities - what the model actually likes

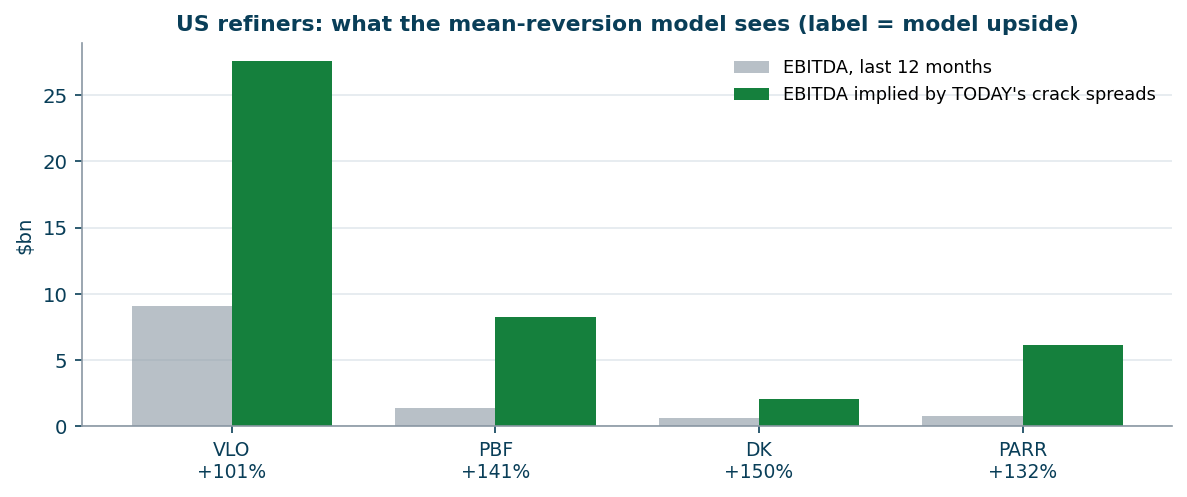

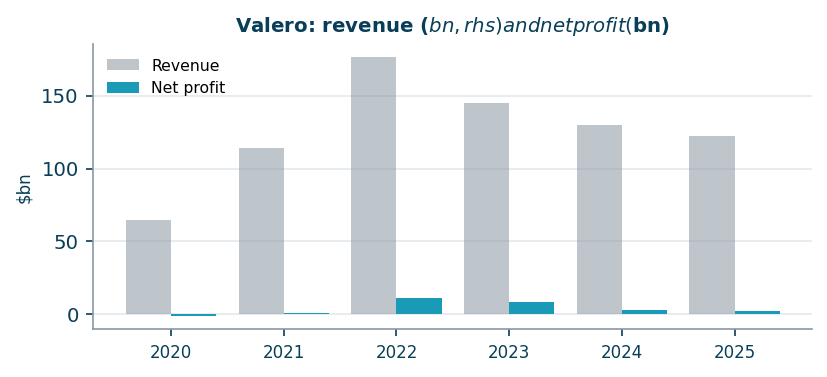

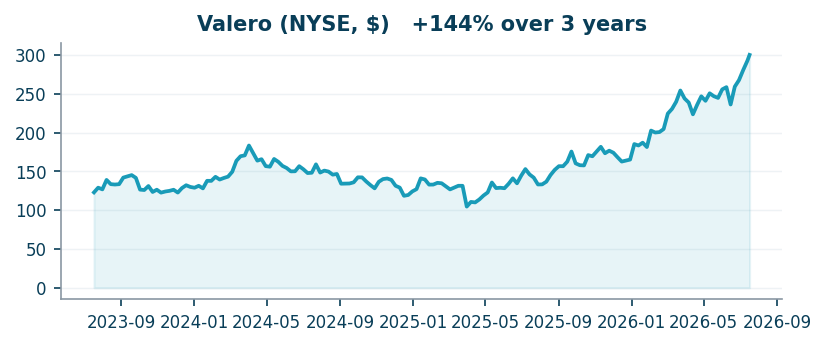

10. Valero (NYSE: VLO) - the quality way to own the refining cycle

The same thesis that made PBF +36% in three weeks, in institutional form. PBF (+141% model upside) stays the aggressive pure-play; DK (+150%) and PARR (+132%) are the small-cap tail. Risks: crack normalization, product imports.

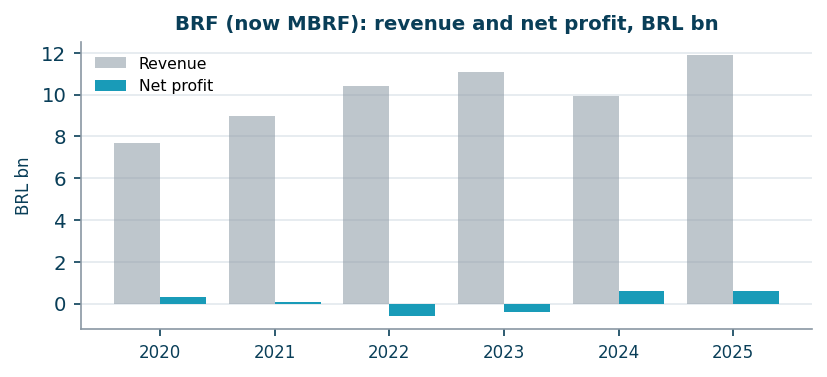

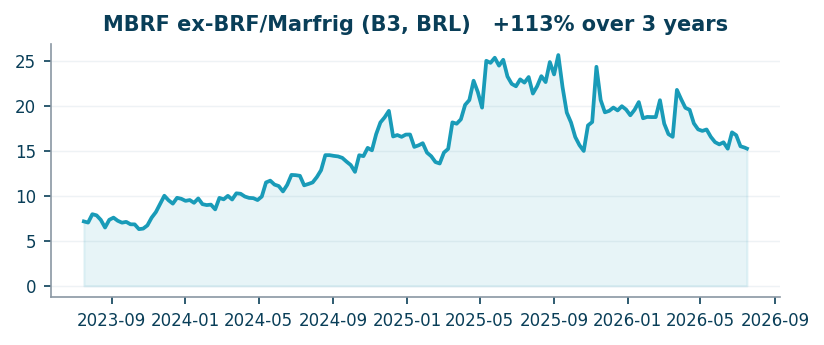

11. MBRF (B3: MBRF3, ex-BRF + Marfrig) - the new global protein giant

Cheap corn, a weak real and merger synergies compound Brazilian chicken's global cost advantage. Risks: US beef cattle cycle, controlling-shareholder governance, BRL.

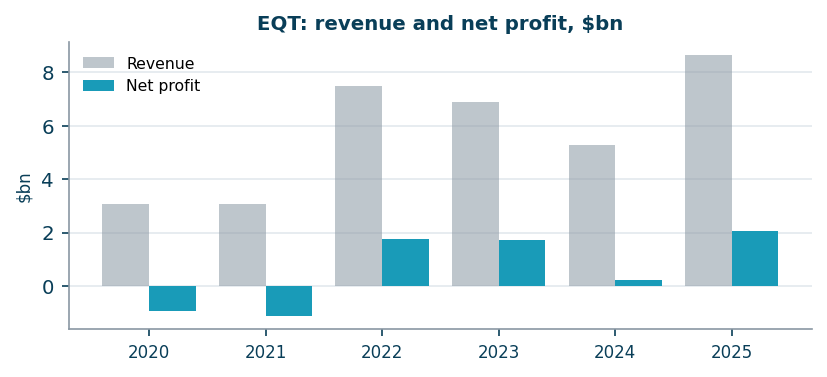

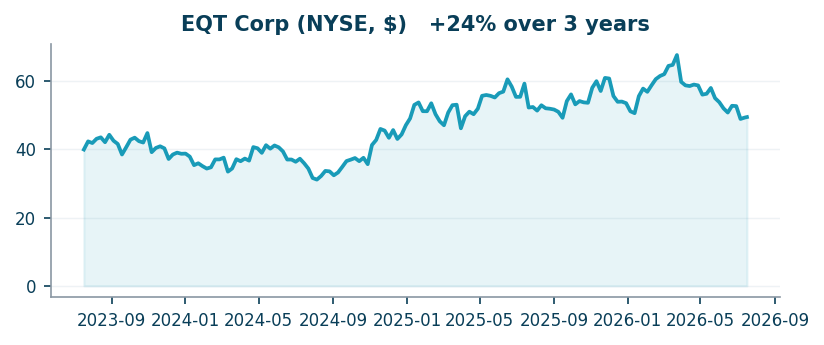

12. EQT (NYSE: EQT) - the structural natural gas winner

Not mean-reversion but a multi-year demand story; the latest quarter already beat on volumes and prices. Risks: gas volatility, LNG contracting.

Part V. US Leaders

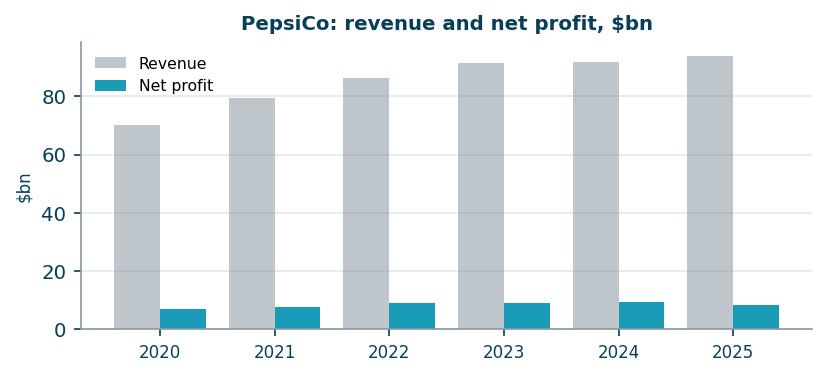

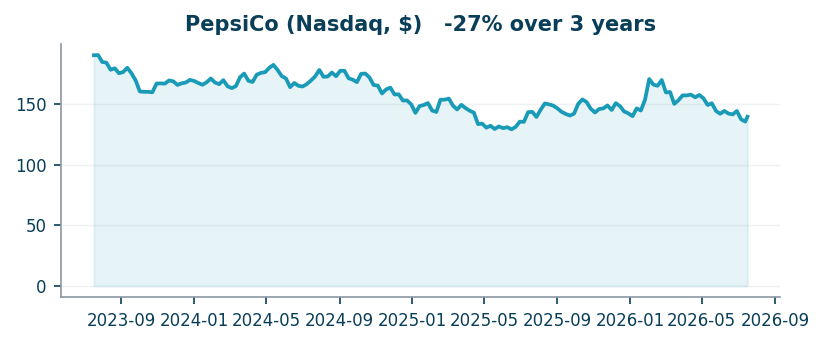

13. PepsiCo (Nasdaq: PEP) - a dividend king at a decade-high yield

GLP-1 fears pushed a pricing-power franchise to its highest yield in decades; the dividend streak is a hard floor, volume recovery is upside. Risks: structural GLP-1 drag, weak US consumer.

Summary

Three baskets. Buy-now via any US broker: BMRI (PPERY), BBRI (BKRKY), KSPI, TLK, PHI, GFNORTEO (IB direct Mexico), VLO, EQT, PEP. Local-access watchlist: CPIN, INDF (Jakarta), MBRF (B3), KEGOC (KASE). Published and running: PBF +36% since June 25.

Prepared by Enhanced Investments, July 2026, from primary filings, exchange and central-bank data. Live track records, not backtests. Not investment advice.

Open the company's financial profile IDEAS →

See also: market overview · valuation map · stock screeners