Refiners after the record: PBF's blowout quarter, the crack-spread turn, and what is actually priced in

Since this idea was published on 25 June, PBF Energy has returned 45% and refining margins have printed an all-time high. Both facts are now history: the crack spread peaked in late July and has since given back a quarter. This update rebuilds the case on fresh data - the Q2 report of 3 August, the margin cycle in five-year context, and a sensitivity model that answers the only question that matters: what crack spread does today's share price actually assume?

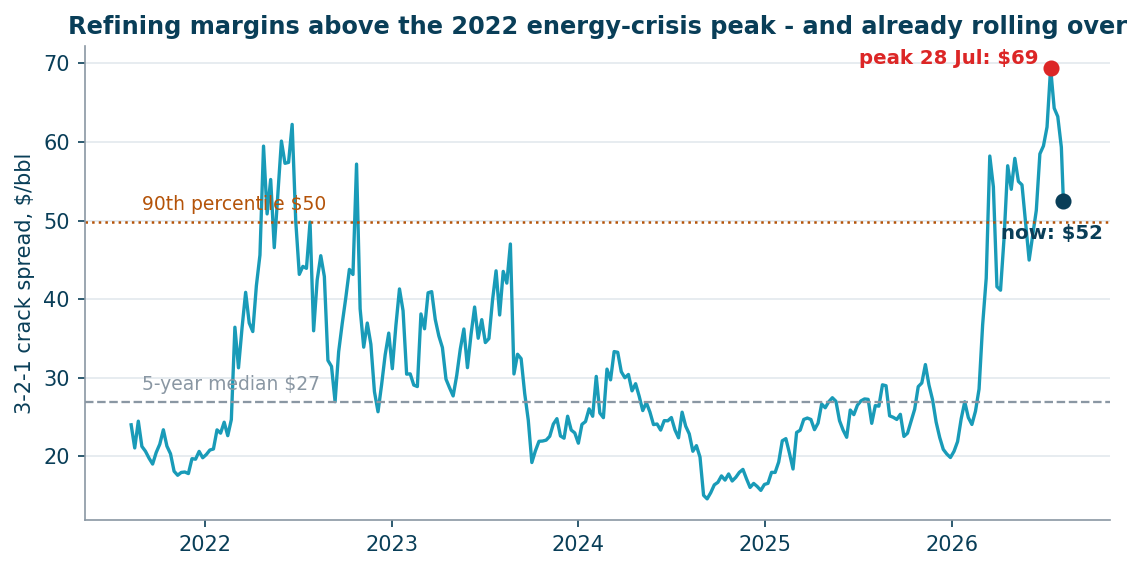

The margin cycle: above the 2022 crisis peak, and already turning

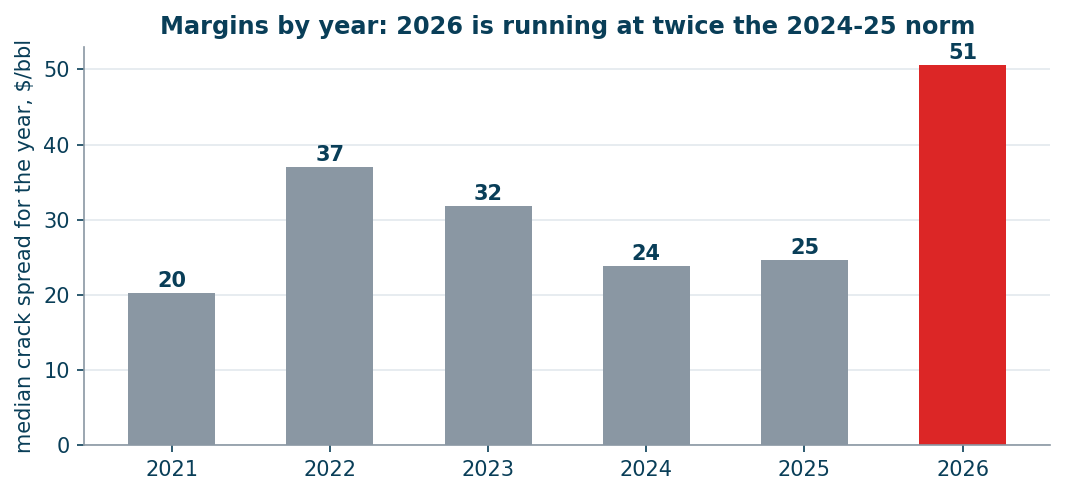

The 3-2-1 crack spread - the standard proxy for refining margin, three barrels of crude turned into two of gasoline and one of distillate - reached about $70/bbl in late July, above the June-2022 record set during the European energy crisis. It now sits near $52. That is a 27% pullback, and it is the fact behind the question we were asked. But the level still matters more than the direction: $52 is the 93rd percentile of the past five years, against a five-year median of $27 and a 2024-2025 norm of $24-25. Margins are not normal; they are twice normal and coming off an extreme.

Why margins went to a record: four constraints at once

This is not a single-shock story. Four supply constraints are active simultaneously: Middle East conflict disrupting Gulf product exports, Russia's diesel export ban extended through 2027, a decade of structural refinery closures in the West, and China's restrictive fuel export quotas. The result is record margins against multi-decade-low product inventories in the US and Europe. On the capacity side the picture is equally tight: global refining capacity grows only 0.7-1.0 million barrels a day in 2026 - roughly matching demand growth in a year without crises - while roughly a fifth of the world's 420 refineries face closure risk by 2035 as electric-vehicle penetration erodes long-run gasoline demand and carbon compliance costs rise.

The Q2 report: a record quarter, and it is a rear-view mirror

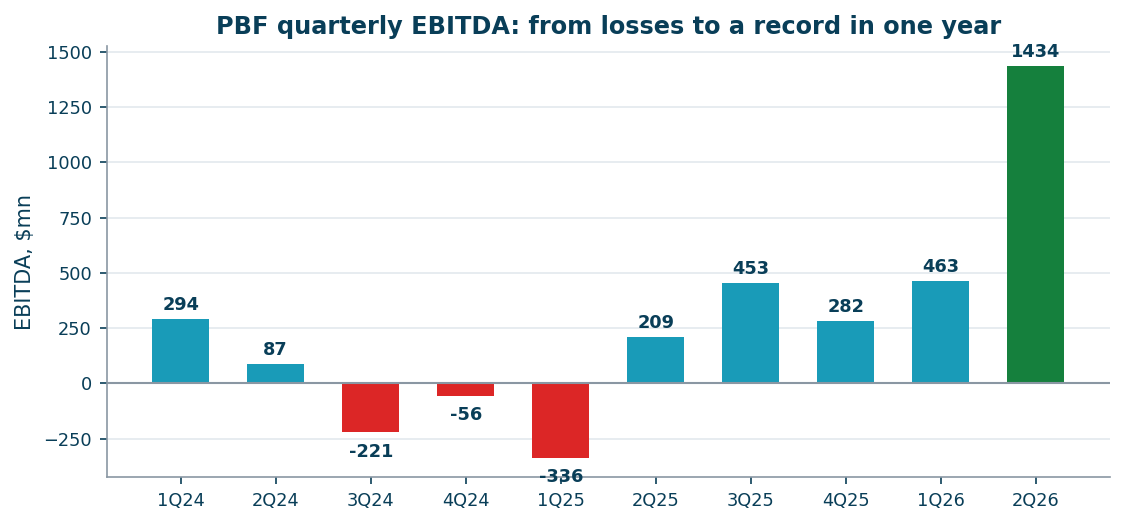

PBF reported on 3 August: adjusted earnings of $6.22 per share against a $4.05 consensus - a 54% beat - on revenue of $11.68bn, up 56% year on year. Adjusted EBITDA came in at $1,240mn against $70mn a year earlier, an eighteen-fold swing; income from operations excluding special items was $1,054mn against a $110mn loss. Throughput rose to 887,300 barrels a day and the Q3 guide is higher still at 900,000-960,000. The Martinez refinery, offline after the February 2025 fire, has been at full rates since May. Net debt is down to $855mn against cash of $894mn, and the dividend is back at $0.275 a quarter. Peers tell the same story: Valero posted its most profitable quarter on record by earnings per share, with net income of $3.7bn against $714mn a year earlier.

The peak-earnings trap - and why the usual conclusion is wrong here

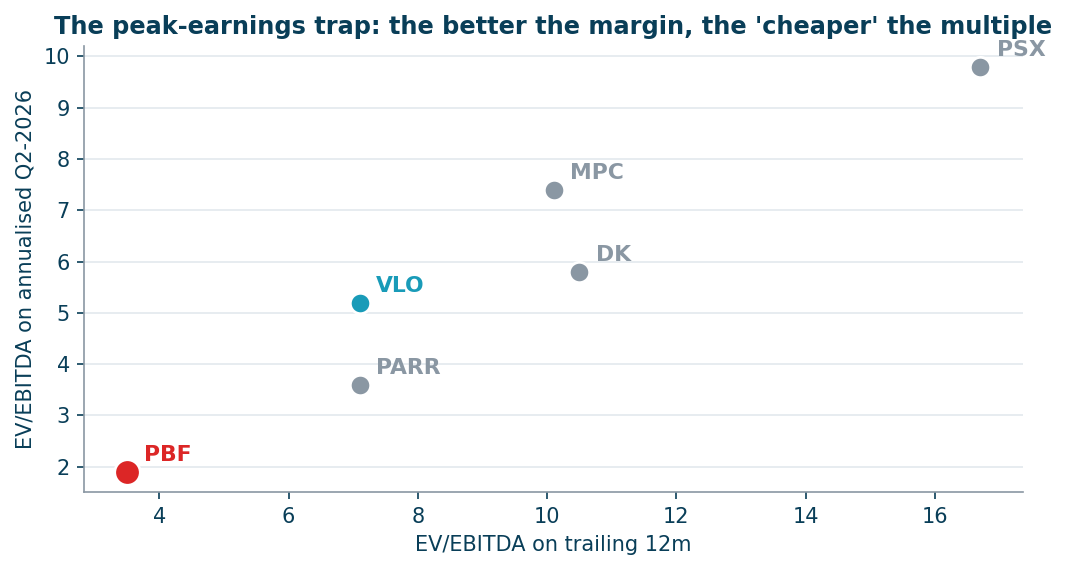

The textbook rule for cyclicals says a low multiple on peak earnings is a sell signal, not a bargain. PBF trades at 3.5x EV/EBITDA on the trailing year and about 1.9x on the annualised second quarter - exactly the configuration that rule warns about. But applying the rule blindly here would be a mistake, because it assumes the market is paying for peak margins. It is not.

What the share price actually assumes: a crack spread of $31-38

PBF's earnings track the crack spread closely enough to model directly. Regressing the last ten quarters of EBITDA on the average crack spread of each quarter gives quarterly EBITDA of roughly minus $1,100mn plus $50mn for every dollar of crack spread, with an R-squared of 0.90. The fit is not academic: it predicts $1,445mn for the second quarter against the $1,434mn actually reported. Inverting it against the current share price of $61.2 - 126.8mn shares, $249mn of net debt on the guided balance sheet, an exit multiple of 4x - implies annual EBITDA of about $2.0bn, which corresponds to a crack spread of $32.1. Across a plausible range of exit multiples from 3.2x to 5x, the implied crack is $30-35. In other words the market is already pricing a return to roughly the five-year median, not the $57 of today or the $70 of late July.

The call added three things the release did not

The first is the balance sheet, which moved further than the quarter-end numbers suggest. Net debt fell by $1.4bn during the quarter to a net-debt-to-capital ratio of 15%, down from 36% three months earlier, helped by a fifth insurance payment of $250mn that brought total recoveries for the Martinez fire to $1.25bn net of deductibles. Management expects one more payment of similar size and guided to roughly $1.5bn of cash by 31 July - against $1,749mn of debt that implies net debt near $250mn, a third of the $855mn on the quarter-end balance sheet. A company that was a leveraged refinery operator two years ago is close to net cash.

The second is that the earnings power is structurally higher than the historical record implies. The cost programme has renegotiated more than half of sixty-plus contracts for chemicals, maintenance and rentals, targeting $60mn of annual savings, and energy efficiency work has cut purchased natural gas per barrel by 20% against a 2024 baseline. Capital spending for 2026 has been guided down to about $850mn at the midpoint, some $75mn lower, by deferring the Toledo and Chalmette turnarounds into 2027. All of this sits outside the regression above, which is fitted on quarters when Martinez was down and none of these savings existed - so the model understates what the company earns at any given margin, and the deferral means 2027 carries the maintenance bill instead.

The third is the most important for anyone sizing a position: PBF does not hedge. Asked directly why the company was not locking in extraordinary cash generation, the chief executive said hedging three months ago would have meant, in his words, getting 'our face ripped off', and framed the policy as delivering 'the crack to our investors'. That is an honest answer and a deliberate choice, but it means the downside scenarios in this note arrive undiluted - there is no hedge book to cushion a margin collapse, unlike the gas producers we reviewed last month. Capital returns are also further away than the cash pile suggests: the stated priority order is investment, then balance sheet, then shareholders, and on buybacks management declined to commit, saying it does not 'openly speculate about money we haven't earned yet'. Idled units at Paulsboro - the fluid catalytic cracker, alkylation unit and coker - stay idled for the same reason: restarting takes long enough that it requires confidence the cycle will outlast the restart.

Management's own read on margins is consistent with the futures curve rather than with the spot level: crude, in the chief executive's framing, 'can and will normalize much quicker than products' - weeks to months for crude against months to quarters for products - with more than five million barrels a day of global refining capacity offline and utilisation down about 10% year on year providing what he called a favourable restocking backdrop. In plain terms, the company expects elevated margins through 2027 and does not argue for the current level persisting.

What multiple is fair here - and why it is far below the market's

Any answer built on capitalising a normalised year depends on the multiple applied, so it deserves its own evidence rather than an assumption. Over the past five years PBF's own trailing EV/EBITDA has had a median of 3.2x. Its peers sit higher: Par Pacific at 5.6x, Valero at 6.9x, Delek at 7.3x, Marathon at 7.8x, Phillips 66 at 9.8x. Against the broad US market, where the S&P 500 trades in the mid-teens, all of these look extraordinarily cheap - and that is not an anomaly waiting to correct. Refining is capital-intensive, violently cyclical, and carries terminal-value risk as electric vehicles erode gasoline demand; the sector has traded at a structural discount for a decade.

Within that cheap sector PBF sits at the bottom, and for identifiable reasons rather than neglect. It is a pure-play refiner: no retail network, no midstream partnership of the kind that carries a premium multiple at Marathon or Phillips 66, no renewables business at scale. Its balance sheet is high-yield rated. Its asset base is older and more complex, with heavy California exposure - Martinez and Torrance - where regulation is tightest and where the February 2025 fire took a refinery offline for over a year. And at roughly $8bn of market value it is a fraction of Valero's size, with the liquidity and beta that follow. A pure-play, sub-investment-grade, California-exposed refiner does not earn a Marathon multiple, and pricing one into a valuation would be wishful. Using 4x for the scenarios above is therefore already generous relative to the company's own history.

The honest consequence cuts against the position. At PBF's own median multiple of 3.2x and the Cal-2028 strip of $33.7, fair value is about $56 a share on the guided balance sheet - some 8% below today's $61. At the same multiple but the Cal-2027 strip of $41.0, it is $91, half as much again. The stock is therefore not obviously cheap or obviously expensive; it sits between a normalised-2028 valuation and a 2027 one, and which of those the next twelve months resemble is precisely what nobody knows.

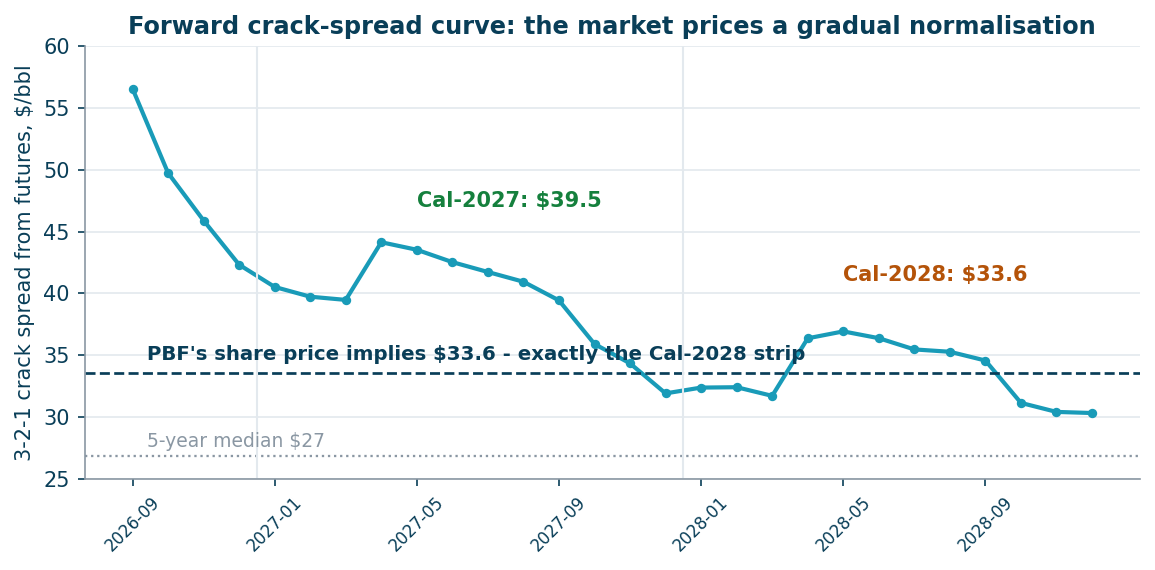

The futures curve says the same thing - and dates it

The equity-implied number can be checked against a market that trades the margin directly. Building the 3-2-1 crack from the futures strip - gasoline, distillate and crude contracts for the same delivery month - gives a curve in steep backwardation: about $59 for September 2026, sliding from $52 in October to $45 in December, an average of $41.0 across calendar 2027 and $33.7 across calendar 2028. Set against the equity-implied number, the curve says the market is capitalising a margin somewhere between the 2027 and 2028 strips: inverting the regression gives $34.6 at PBF's own historical multiple of 3.2x, $32.1 at 4x and $29.2 at 5.6x. Two independent markets - equities and futures - therefore agree on the substance, that a normalised margin is what is being paid for, while the exact year depends on the multiple one considers fair.

This reframes the whole question. The share price is not discounting today's margin, and it is not discounting next year's either - it is discounting the margin the market expects two and a half years out, and giving no credit for the eighteen months of elevated cash flow in between. On curve prices and the same regression, PBF earns roughly $4.8bn of annualised EBITDA in the second half of 2026, $3.5bn across 2027 and $2.3bn in 2028. Against an enterprise value of $9.3bn that is 1.9x, 2.7x and 4.0x respectively: at 4x the stock is valued off the normalised year with the two strong years in front of it free - though at the company's own 3.2x that cushion largely disappears, which is why the multiple question above is not academic. The obvious caveat is that a forward curve is not a forecast - crack futures are thin beyond a year and are habitually dragged toward spot, so the 2028 level says more about where hedgers will transact than about where margins will actually settle.

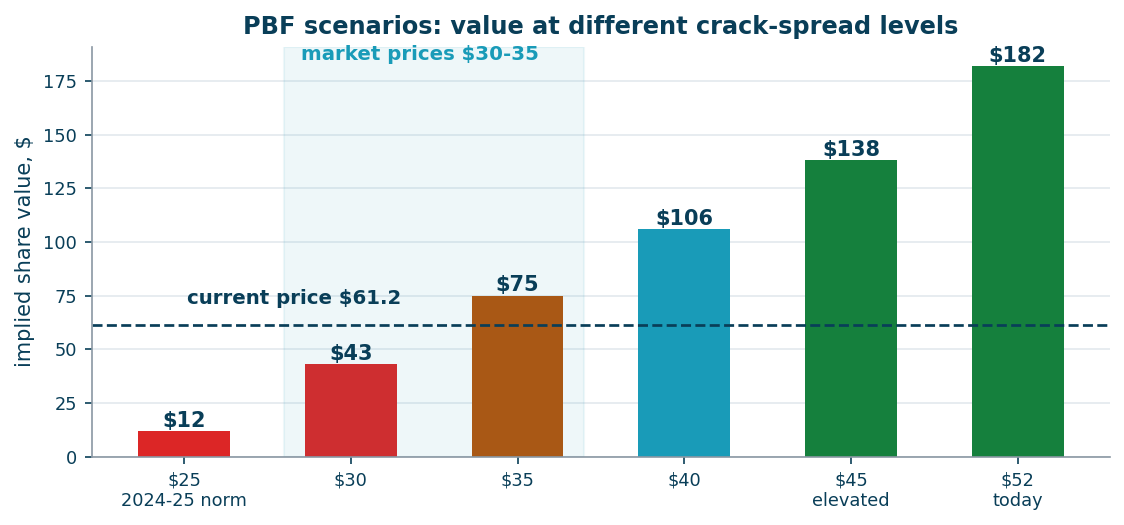

The scenario table that follows from the same model is violently two-sided. At a crack spread of $25 - the 2024-2025 norm - the equity is worth about $12 a share, an 82% loss, because PBF's cost base leaves almost nothing at that margin: the company posted EBITDA between minus $336mn and plus $453mn in exactly those conditions. At $35 the value is $75, slightly above today's price. At $40 it is $106, at $45 it is $138. One caveat runs in the investor's favour: the regression is fitted over a period when Martinez was offline for more than a year, so current earning power at any given margin is understated by the fit.

Risks - the ones that actually move this

De-escalation in the Middle East is the single largest one: much of the current margin rests on disrupted Gulf product flows, and a settlement removes it quickly. Second, the same structural closures that support margins invite a supply response - refiners are expected to lift gasoline yields through the second half of 2026, and global capacity additions, though modest, are real. Third, demand: a US or European recession hits distillate first, and distillate is where the current tightness lives. Fourth, company-specific: PBF's operating leverage cuts both ways, as the $25 scenario shows, and the Martinez restart concentrates a large share of earnings in one asset that has already had one fire. Finally, this is a single-variable model - it holds crude differentials, opex and turnaround schedules constant, and all three move.

Capitalising one year throws away the transition - so value the path

Every multiple-based answer above shares one flaw: it capitalises a single normalised year and ignores what the company earns on the way there. If margins really do slide from $52 today to $41 next year and $34 in 2028, PBF still collects two and a half years of unusually high cash first, and that cash has value. A discounted cash-flow model built on the futures strip captures it. Taking EBITDA from the same regression, subtracting the guided capital programme - about $500mn in the second half of this year, roughly $1.05bn in 2027 when the deferred Toledo and Chalmette turnarounds land, $850mn in 2028 - along with $660mn of depreciation, net interest of about $45mn and cash tax at 22% with no credit for accumulated losses, the path produces free cash flow of $2.09bn in the second half of 2026, $2.01bn in 2027 and $1.08bn in 2028.

That is $5.2bn of free cash flow over two and a half years against a market capitalisation of $7.8bn - two thirds of the equity value returned in cash before any terminal assumption is made. It is the strongest fact in the bull case and it is precisely what a one-year multiple discards.

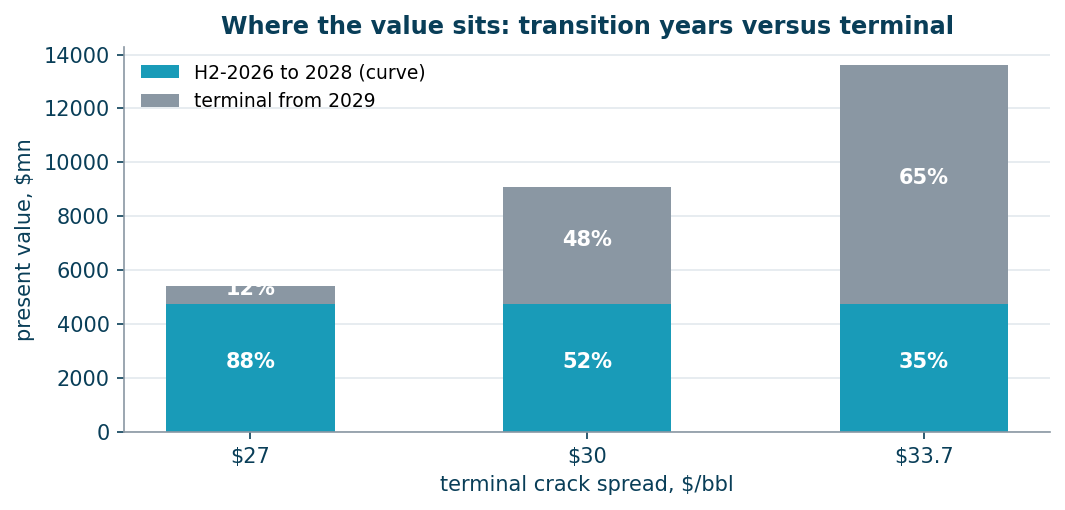

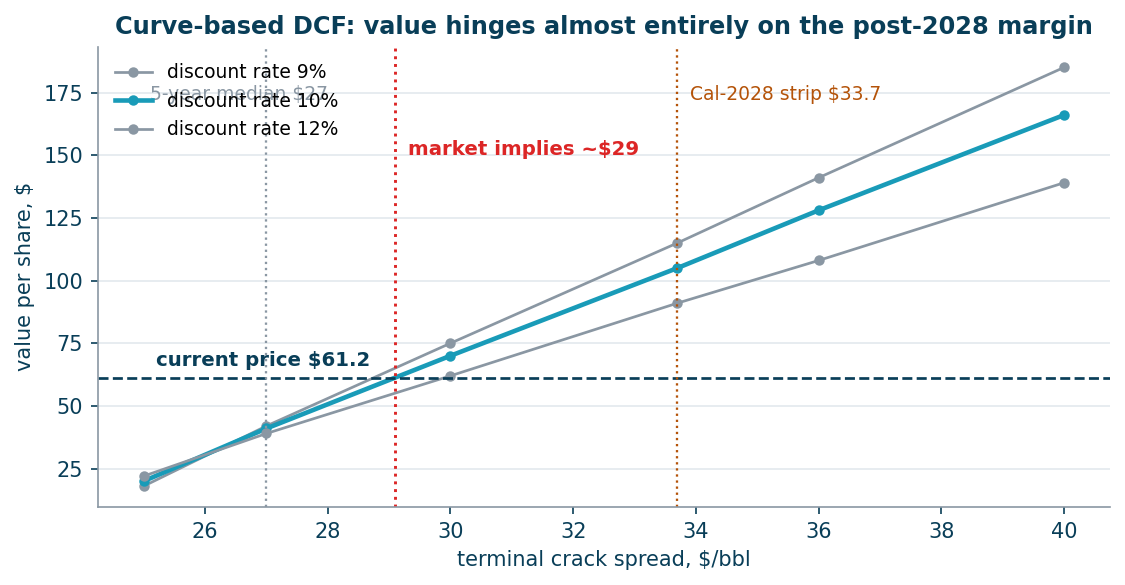

What the model then shows is that everything still turns on the margin after 2028. Discounting at 10% and assuming no real growth in perpetuity - reasonable for an industry facing gradual demand erosion - the value per share is $20 at a terminal crack of $25, $41 at $27, $70 at $30, $105 at $33.7 and $166 at $40. The current price of $61.2 corresponds to a terminal margin of $29. That is a lower implied margin than the multiple method suggested, and the reason is precisely the transition: once the interim cash is counted, a smaller long-run margin is enough to justify the price.

The composition of that value is the sharpest way to frame the risk. If the long-run margin returns to the five-year median of $27, the transition years account for 88% of the entire valuation - the business beyond 2028 is worth almost nothing, because at that margin PBF barely covers maintenance capital - and the shares are worth $41 against $61 today. At $30 the split is even, half transition and half terminal. At the Cal-2028 strip of $33.7, two thirds of the value sits in the terminal period and the shares are worth $105. The investment case is therefore not a view on this year's margin at all; it is a view on whether the structural constraints - closures, the Russian export ban, tight inventories - hold the long-run margin above roughly $30, three dollars above its own five-year median.

Prepared by Enhanced Investments from PBF Energy's Q2 2026 results (press release of 3 August 2026), peer disclosures, NYMEX futures settlements for the crack-spread series and EIA data; August 2026. The sensitivity model is our own and is described in full above so it can be checked. Not individual investment advice.

Open the company's financial profile PBF →

See also: market overview · valuation map · stock screeners